Market Overview:

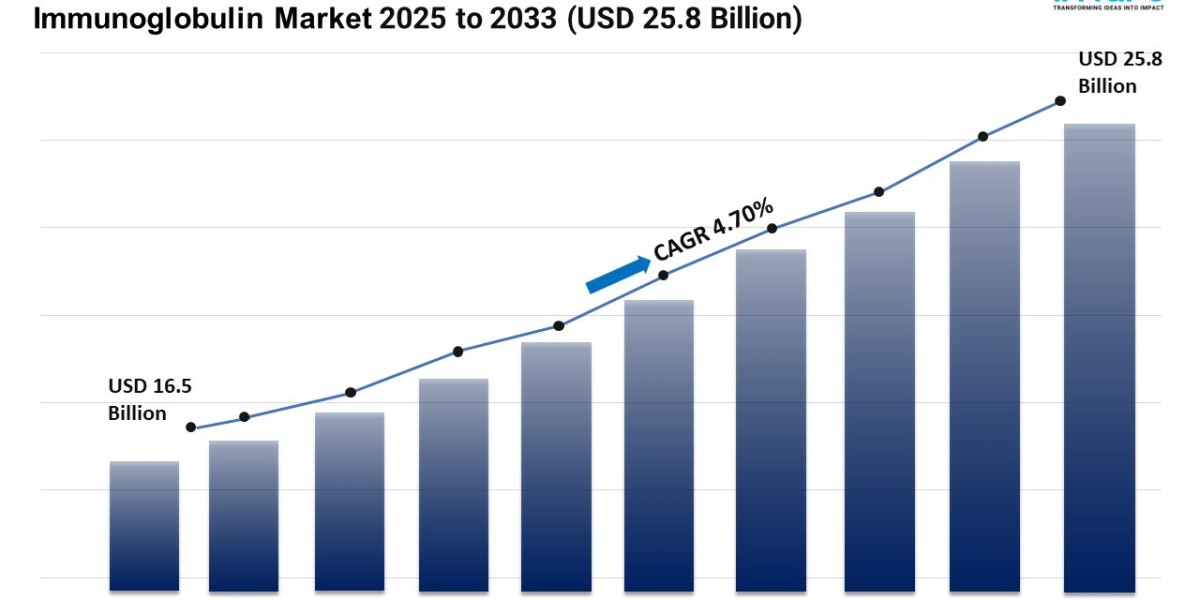

The immunoglobulin market is experiencing rapid growth, driven by rising chronic diseases, biosimilar competition intensifies, and supply chain vulnerabilities. According to IMARC Group's latest research publication, "Immunoglobulin Market :Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global immunoglobulin market size was valued at USD 16.45 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 25.77 Billion by 2033, exhibiting a CAGR of 4.70% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/immunoglobulin-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends And Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Immunoglobulin Industry:

- Rising Chronic Diseases

The global burden of chronic illnesses continues to fuel demand for immunoglobulin therapies. Autoimmune conditions like lupus, multiple sclerosis, and rheumatoid arthritis are seeing higher prevalence rates, while cancer-related immunodeficiencies add further strain on healthcare systems. With elderly populations expanding in Europe, Japan, and North America, immune-related complications are becoming more frequent, necessitating long-term immunoglobulin support. Simultaneously, governments in Asia-Pacific and Latin America are investing in improved diagnostic frameworks, enabling earlier detection of immune deficiencies. The growing emphasis on personalized and precision medicine further reinforces immunoglobulin’s position as a key therapy in chronic disease management worldwide.

- Biosimilar Competition Intensifies

Competition in the immunoglobulin market is escalating with the arrival of biosimilar formulations and novel delivery innovations. Regulatory reforms in the U.S., EU, and Japan are creating a pathway for faster approvals, encouraging companies to invest in affordable alternatives. Startups and regional players are also entering the market, disrupting traditional dynamics once dominated by a few multinational firms. To defend market share, established manufacturers are focusing on patient support platforms, integrated digital monitoring, and innovations like ready-to-use formulations. Strategic mergers, acquisitions, and collaborations are also rising, allowing firms to pool expertise. The resulting competition is expected to drive affordability and expand treatment accessibility.

- Supply Chain Vulnerabilities

The immunoglobulin sector continues to face systemic risks due to its reliance on plasma donations. Any disruption—from pandemics to cross-border trade restrictions—creates shortages that directly impact patients. Many developing nations remain highly dependent on imports, exposing them to volatility in global supply availability. To mitigate risks, companies are investing in regional plasma collection hubs and automated donation systems to enhance efficiency. Additionally, partnerships with hospitals and NGOs are expanding outreach in underserved areas. While recombinant technology is gaining momentum, it is still at an early stage. Addressing these vulnerabilities is crucial to safeguarding patient treatment continuity worldwide.

Key Trends in the Immunoglobulin Market

- Technological Improvements in Plasma Fractionation

Plasma fractionation technology is undergoing a major transformation, with AI, robotics, and digital monitoring enabling unprecedented efficiency. Automation reduces batch variability, ensuring consistent product quality while lowering operational costs. Advanced filtration and purification techniques are improving protein yield, helping manufacturers scale up production to meet global demand. New inline monitoring tools are enhancing compliance with stringent regulatory frameworks in the U.S. and EU. Companies are also experimenting with hybrid models that combine traditional plasma methods with recombinant solutions, enabling flexibility in manufacturing. These technological innovations are making plasma fractionation more sustainable, reliable, and responsive to rising therapeutic needs.

- Shift Toward Subcutaneous Immunoglobulin (SCIG)

SCIG is rapidly gaining traction as a more patient-friendly alternative to intravenous therapies. Home administration, supported by wearable pumps and digital adherence tools, reduces hospital dependency and improves treatment flexibility. Healthcare providers favor SCIG for its lower risk of systemic side effects and better patient compliance, especially among children and elderly populations. Insurance companies and payers are increasingly supportive of SCIG, given its cost-effectiveness through reduced hospitalization. Moreover, research is exploring extended-duration SCIG formulations that allow less frequent dosing. This shift aligns with the broader healthcare trend toward decentralized and personalized treatment, positioning SCIG as a game-changer in the immunoglobulin landscape.

- Focus on Plasma Supply and Donor Recruitment

Ensuring sustainable plasma availability remains a top priority for industry leaders. Governments are working closely with companies to boost donor engagement through awareness campaigns, digital booking systems, and financial rewards. Mobile collection centers are expanding plasma reach into rural and underserved regions, while blockchain platforms are being tested to improve transparency and traceability. AI-driven donor profiling is helping predict retention patterns and optimize recruitment. At the same time, patient advocacy groups are partnering with healthcare providers to raise awareness about plasma’s role in life-saving therapies. By strengthening donor networks, the industry aims to create a stable foundation for future supply.

The immunoglobulin market report provides a comprehensive overview of the industry. This analysis is essential for stakeholders aiming to navigate the complexities of the immunoglobulin market and capitalize on emerging opportunities.

Leading Companies Operating in the Global Immunoglobulin Industry:

- ADMA Biologics Inc.

- Baxter international Inc.

- Biotest AG

- CSL Limited

- Grifols S.A

- Kedrion S.p.A

- LFB SA

- Octapharma AG

- Sanquin Plasma Products B.V.

- Takeda Pharmaceutical Company Limited

Immunoglobulin Market Report Segmentation:

Breakup By Product:

- IgG

- IgA

- IgM

- IgE

- IgD

IgG represents the largest segment as IgG is the most abundant immunoglobulin in human serum and is widely used for various therapeutic applications.

Breakup By Application:

- Hypogammaglobulinemia

- Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- Immunodeficiency Disease

- Myasthenia Gravis

- Others

Immunodeficiency disease accounts for the majority of the market share. Immunodeficiency diseases require ongoing treatment with immunoglobulin therapies, resulting in a substantial demand that accounts for a significant portion of market share.

Breakup By Mode of Delivery:

- Intravenous Mode of Delivery

- Subcutaneous Mode of Delivery

Intravenous mode of delivery exhibits a clear dominance in the market due to its rapid administration and higher plasma levels of immunoglobulin, making it the preferred method for many clinicians and patients.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the immunoglobulin market on account of its well-established healthcare infrastructure, higher prevalence of immunodeficiency diseases, and greater access to advanced treatment options.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States:+1–201971–6302