IMARC Group, a leading market research company, has recently released a report titled "Sickle Cell Disease Treatment Market Report Size, Share, Trends and Forecast by Treatment Type, End User, and Region, 2025-2033." The study provides a detailed analysis of the industry, including the global sickle cell disease treatment market share, size, trends, growth and forecast. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Market Overview

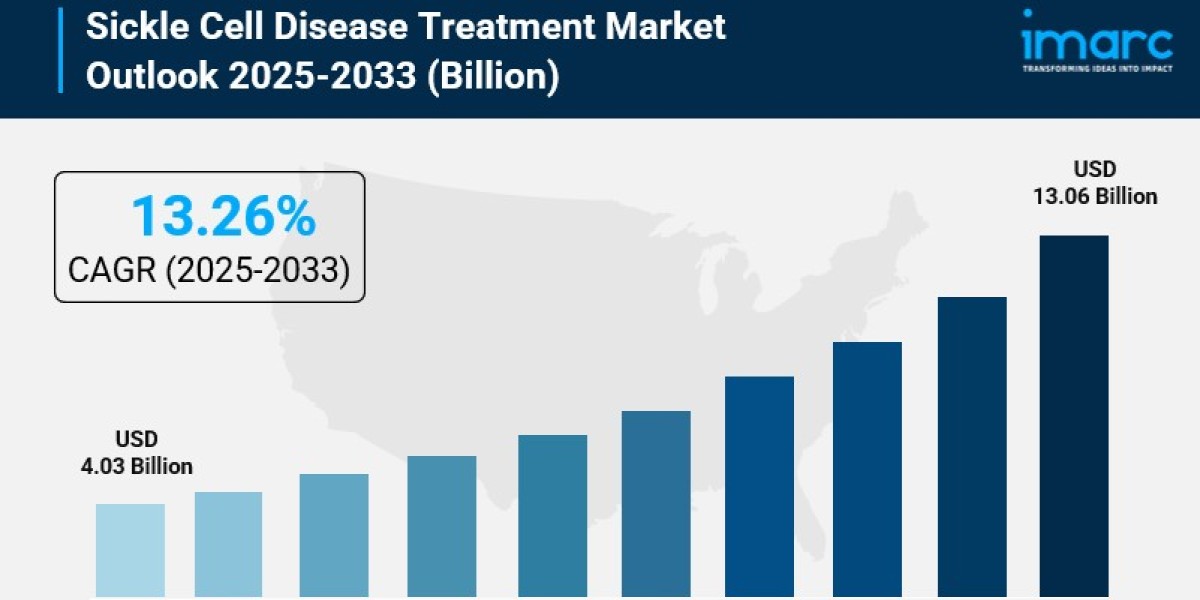

The global sickle cell disease treatment market size was valued at USD 4.03 Billion in 2024 and is expected to reach USD 13.06 Billion by 2033, growing at a CAGR of 13.26% during the forecast period 2025-2033. The market growth is driven by rising prevalence of sickle cell disease, expanding newborn screening programs, advancements in gene and cell therapies, and supportive government policies. North America dominates with about 38.7% market share in 2024, supported by advanced healthcare infrastructure and high disease awareness.

Study Assumption Years

- Base Year: 2024

- Historical Year/Period:2019-2024

- Forecast Year/Period2025-2033

Sickle Cell Disease Treatment Market Key Takeaways

- Current Market Size: USD 4.03 Billion (2024)

- CAGR: 13.26%

- Forecast Period: 2025-2033

- North America holds the largest share with 38.7% in 2024, driven by advanced healthcare infrastructure and strong research.

- Blood transfusion leads the treatment type segment with 48.9% share due to its widespread use and efficacy.

- Hospitals are the largest end-user segment with 60.8% share, offering comprehensive disease management.

- Rising prevalence globally, especially in regions like Africa, Asia-Pacific, and Latin America, fuels market demand.

- Growing government and private funding is accelerating research and novel therapies, notably gene editing.

Request Your Free “Sickle Cell Disease Treatment Market” Insights Sample PDF: https://www.imarcgroup.com/sickle-cell-disease-treatment-market/requestsample

Market Growth Factors

The growth in the sickle cell disease treatment market can be attributed to growing prevalence. More than 20 million people are projected to have SCD globally in 2025, concordant with over 100,000 cases in the US. This is mainly due to the growing population of countries with a heavy disease burden combined with newborn screening programs that expand the number of cases detected at birth. With migration these diseases spread to other parts of the world. Because of increased life expectancy furthermore, there is a higher proportion of patients that have complications that require other curative/supportive therapies. Governments and healthcare providers should adapt to the growing number of patients through expanded treatment infrastructure and sped therapy development.

The rising disposable income in developing countries supports the adoption of SCD treatment. The disposable personal income level in the US reached USD 22,454.6 Billion around May 2025. Patients can afford specialized medical care with frequent tests and scans costly new drugs like gene therapies. Governmental campaigns, advocacy groups, and educational initiatives increased public awareness of the disease's signs and symptoms. More patients participate in clinical trials for learning about new therapies within. Improved financial capacity and awareness both expand the primary market and help create demand for therapies.

It is a positive trend that accelerated drug approvals have been made in several countries. In 2019, US FDA approved a drug to decrease SCD pain occurrences. Use of priority review, breakthrough therapy and orphan drug designations accelerated the development process and gave patients early access to experimental gene or cell-based treatments. Regulators were meeting up-front with developers to make sure trial design, safety and manufacturing met requirements, while balancing safety with the need for innovation. This has the positive effect of reducing risks and increasing returns on investment, further helping the market.

Market Segmentation

Breakup By Treatment Type:

- Blood Transfusion: Constitutes the largest treatment segment with 48.9% share in 2024. It reduces sickled red blood cells, improving oxygen delivery and preventing severe complications. It is critical in managing acute episodes and preventing crises and is utilized as a long-term preventive measure.

- Pharmacotherapy

- Bone Marrow Transplant

Breakup By End User:

- Hospitals: Leading end-user segment with 60.8% market share in 2024. Hospitals provide comprehensive diagnosis, acute and preventive care, specialized treatments like stem cell transplant and gene therapy, and patient education.

- Diagnostic Centers

- Others

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America leads the market with over 38.7% share in 2024, attributed to advanced healthcare infrastructure, established screening programs, high disease awareness, and strong research capabilities. Favorable reimbursement policies and government-funded healthcare improve access to a wide range of therapies, from supportive to advanced gene and cell therapies. The region’s leadership is reinforced by specialized treatment centers and continuous clinical research facilitating rapid adoption of innovative treatments.

Recent Developments & News

- June 2025: Ministry of Tribal Affairs and AIIMS Delhi launched a drug development competition for sickle cell disease targeting India’s tribal populations, with assurance of full funding and free medicine support.

- June 2025: Beam Therapeutics received orphan drug designation from the U.S. FDA for BEAM-101, a genetically modified cell therapy for sickle cell disease.

- May 2025: Indian Council of Medical Research introduced the ICMR-SCD Stigma Scale tailored to India’s socio-cultural context to address patient and caregiver stigma.

- March 2025: UCSF Benioff Children’s Hospital Oakland initiated a clinical trial using CRISPR-Cas9 gene editing aiming for sickle cell disease cure.

- February 2025: The first gene-editing therapy for sickle cell disease using CRISPR technology was developed, offering hope for patients suffering frequent pain episodes.

Key Players

- AstraZeneca Plc

- Baxter International Inc.

- bluebird bio Inc.

- Bristol-Myers Squibb Company

- CRISPR Therapeutics

- Emmaus Medical Inc.

- Global Blood Therapeutics Inc.

- GlycoMimetics Inc.

- Novartis AG

- Pfizer Inc.

- Sangamo Therapeutics

Ask Analyst For Request Customization: https://www.imarcgroup.com/request?type=report&id=4076&flag=E

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201971-6302